RRSP Withdrawal Tax Calculator 2026: How Much Will the CRA Take?

For many Canadians, the Registered Retirement Savings Plan (RRSP) is a "black box." You put money in, you get a tax refund, and you forget about it until age 65.

But in 2026, with the cost of living spiking and mortgage renewals looming, thousands of Canadians are cracking that box open early. Whether it’s to pay down high-interest debt, cover an emergency, or fund a gap year, the search for "early RRSP withdrawal" is trending higher than ever.

Here is the reality check: The bank will not give you all your money.

Before the cash ever hits your account, the government takes an immediate "haircut" known as the Withholding Tax. This is not a penalty—it is a prepayment of income tax. However, the confusion between this immediate tax and your actual final tax bill leads to thousands of Canadians owing the CRA money unexpectedly in April.

This is the Official 2026 Guide to RRSP Withdrawals. We break down the exact 10%, 20%, and 30% brackets, the "Quebec Exception," and the street-level strategies to access your funds without triggering a CRA audit.

RRSP Withdrawal Estimator 2026

1. The 2026 Withholding Tax Trap

The most common misconception about RRSPs is that you can withdraw small amounts tax-free. This is false. Every single dollar you remove from an RRSP is considered "Taxable Income" in the year you receive it.

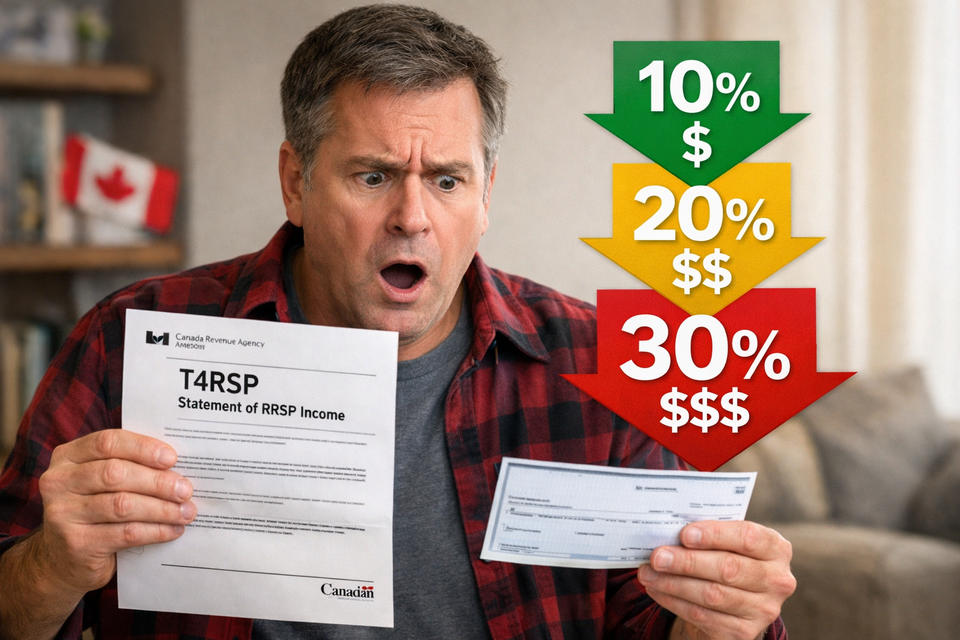

Because the CRA knows you might spend the money before tax season, they force the bank to deduct taxes immediately. This is called the "Withholding Tax," and in 2026, the brackets are rigid.

The 10-20-30 Rule (All Provinces Except Quebec)

The withholding rates are tiered based on the size of your withdrawal request. The larger the withdrawal, the bigger the immediate hit.

- Tier 1: Up to $5,000

- Tax Withheld: 10%

- The Math: If you ask for $5,000, the bank keeps $500. You receive **$4,500**.

- Tier 2: $5,001 to $15,000

- Tax Withheld: 20%

- The Math: If you ask for $15,000, the bank keeps $3,000. You receive **$12,000**.

- Tier 3: Over $15,000

- Tax Withheld: 30%

- The Math: If you ask for $30,000, the bank keeps $9,000. You receive **$21,000**.

Warning: These rates are just "Pre-Payments." If your regular job puts you in a 40% tax bracket (check the 2026 Canadian Tax Brackets to confirm your rate), the bank will only take 30% today, but you will owe the remaining 10% when you file your taxes in April. This is the "Tax Gap" that blindsides high earners.

The Quebec Exception

If you live in Quebec, the rules are more aggressive because you have to satisfy both Revenu Québec and the CRA instantly. Quebec residents face a combined withholding tax that is significantly higher for small withdrawals.

- Up to $5,000: 20% total tax (5% Federal + 15% Provincial).

- $5,001 to $15,000: 25% total tax (10% Federal + 15% Provincial).

- Over $15,000: 30% total tax (15% Federal + 15% Provincial).

2. Street Strategies & "Hacks" Explained

Can you avoid the tax? Is there a loophole? Here is the technical breakdown of the common "Street Strategies" discussed on forums in 2026.

Strategy A: The "$5,000 Split" Maneuver

The most popular "street" strategy is trying to stay in the 10% bracket to maximize cash flow today.

- The Theory: Instead of withdrawing $10,000 (which triggers a 20% tax), you withdraw $5,000 today and $5,000 next week.

- The Reality: This works for immediate cash flow only. You get more money in your pocket today because only 10% is withheld on each transaction.

- The Trap: Financial institutions are legally required to track "series of withdrawals." If you make multiple requests in a short period (e.g., 24 hours), the system often aggregates them and applies the higher 20% rate retroactively or on the second transaction. Furthermore, this does not save you actual tax; you will still owe the full amount at tax time based on your total annual income.

Strategy B: The "Low-Income Year" Strategy

The only mathematically sound way to reduce RRSP tax is to withdraw during a "Low-Income Year."

- The Strategy: If you are laid off, taking a sabbatical, or on maternity leave in 2026, your total income might drop to $30,000.

- The Result: Your marginal tax rate drops to the lowest bracket (approx. 20%). Since the bank withheld 10% or 20%, you likely won't owe any extra money at tax time—you might even get a refund. If you do overpay, check our guide on CRA Refund Status "Assessed" but No Money to track when you will get that cash back.

- The Move: Never withdraw RRSP money in a year where you got a bonus or a raise. Save withdrawals for years where you earn less than $55,000.

Strategy C: The HBP/LLP "Tax-Free" Shield

There are only two legal ways to withdraw RRSP funds without triggering any withholding tax.

- Home Buyers' Plan (HBP): You can withdraw up to $60,000 tax-free to buy your first home. You must repay this over 15 years.

- Lifelong Learning Plan (LLP): You can withdraw up to $10,000/year (max $20,000) to go back to school full-time.

- The Hack: If you are eligible for the HBP, use it. It effectively acts as an interest-free loan from yourself. Before doing this, ensure you understand the repayment rules in our HBP Repayment Guide. If you are looking to buy a home but haven't started saving yet, consider the First Home Savings Account (FHSA) instead, as it offers tax-free withdrawals without the need to repay the funds.

3. The "Loss of Room" Penalty

Before you click "Transfer," you must understand the permanent cost.

Unlike a Tax-Free Savings Account (TFSA), where contribution room bounces back the next year, RRSP room is lost forever once you withdraw.

- Example: If you withdraw $10,000 in 2026, you permanently lose that $10,000 of tax-sheltered space. You cannot put it back later unless you generate new contribution room from working.

- The Verdict: If you have funds in both accounts, always drain the TFSA first.

4. Impact on Government Benefits

Withdrawing from your RRSP doesn't just increase your tax bill; it can slash your government benefits.

The Canada Child Benefit (CCB) Hit

The Canada Child Benefit is calculated based on your "Adjusted Family Net Income."

- The Mechanism: An RRSP withdrawal counts as income. If you withdraw $20,000 from your RRSP, your family income jumps by $20,000.

- The Consequence: This could reduce your monthly CCB payments significantly starting in July of the following year. For lower-income families, the "clawback" on benefits can be as high as 19% of the withdrawn amount. You can verify exactly how much you might lose by checking our Canada Child Benefit (CCB) Payment Dates article to see the current threshold tables.

- The Calculation: Before withdrawing, calculate if the loss of future CCB payments outweighs the immediate cash value.

OAS and GIS for Seniors

If you are over 65, RRSP withdrawals can trigger the OAS Clawback or reduce your Guaranteed Income Supplement (GIS).

- GIS Trap: For every $1 of RRSP income you withdraw, your GIS is reduced by $0.50. This is a massive 50% "tax" on low-income seniors.

- OAS Recovery Tax: If your net income exceeds $93,454 (the 2026 threshold), you will have to repay some of your Old Age Security.

5. How to Report It (T4RSP Slip)

Come tax season (February 2027), your financial institution will mail you a T4RSP slip.

- Box 22: Shows the total amount you withdrew.

- Box 30: Shows the tax they already took (the withholding tax).

- The Process: You enter the total income on your tax return. The tax software calculates the actual tax you owe based on your total earnings. Then, it subtracts the amount in Box 30.

- Scenario A: If you owe less tax than was withheld, you get a refund.

- Scenario B: If you owe more tax (common for high earners), you must pay the difference to the CRA.

Frequently Asked Questions (FAQ)

Q: Can I claim the withholding tax back?

A: Yes. The amount withheld (e.g., the $2,000 on a $10k withdrawal) is considered a "Tax Installment." You will receive a T4RSP slip from your bank. Enter this on your tax return. If your total tax liability is lower than what you paid, the CRA will refund the difference.

Q: How long does an RRSP withdrawal take?

A: It is not instant. While online transfers within the same bank can happen in 24-48 hours, deregistering funds often requires manual processing. Expect 3 to 5 business days for the funds to become "spendable cash."

Q: Can I withdraw from a Spousal RRSP?

A: Yes, but be careful of the "3-Year Attribution Rule." If your spouse contributed to the account in the current year or the two previous years, the withdrawal will be taxed in their hands (at their likely higher tax rate), not yours. To avoid this, you must wait three full calendar years after the last contribution.

Q: Is there a penalty for withdrawing at age 60?

A: No. You can withdraw from an RRSP at any age. The only "penalty" is the tax. However, once you turn 71, you must convert your RRSP to a RRIF or buy an annuity; you can no longer hold the RRSP.

About the Author

Jeff Calixte (MC Yow-Z) is a Canadian labour market researcher and digital entrepreneur specializing in government benefit data and cost-of-living support. As the founder of CanadaPaymentDates.ca and BetterPayJobs.ca, Jeff helps newcomers, students, and workers navigate the Canadian social safety net—from tracking CRA payment schedules to identifying entry-level employment opportunities.

Sources

- Canada Revenue Agency: T4040 RRSPs and Other Registered Plans for Retirement

- Revenu Québec: RRSP Withdrawal Rates (Provincial)

- TurboTax Canada: Understanding RRSP Withholding Taxes

Note

Official 2026 tax brackets and withholding rates are determined by the Canada Revenue Agency (CRA) and provincial governments. While we strive to keep this information current, government policies are subject to change without notice. All data in this guide is verified against official CRA circulars at the time of publication. We recommend confirming the status of your personal file directly via CRA My Account or by calling the CRA benefit line at 1-800-387-1193.