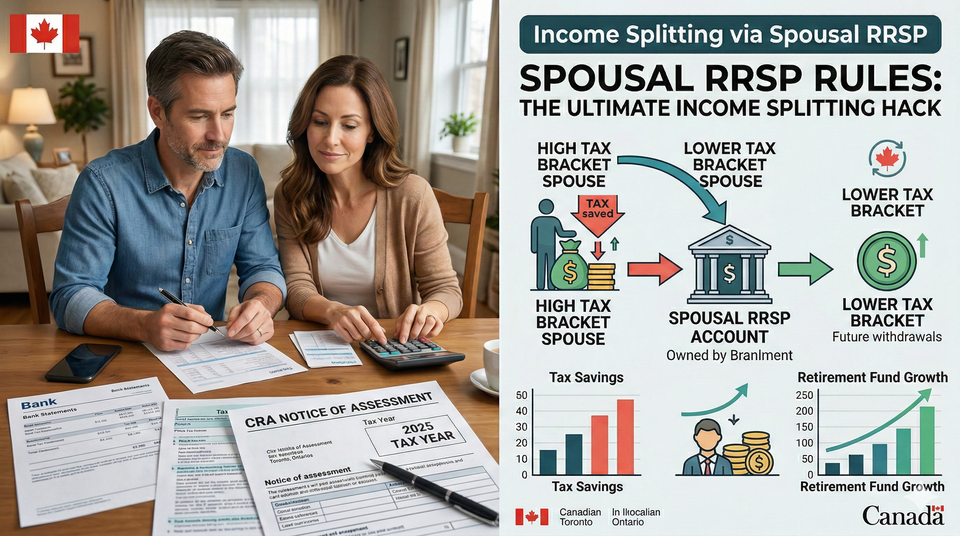

Spousal RRSP Rules 2026: The Ultimate Income Splitting Hack

Canada’s tax system is notoriously harsh on single-income households and couples with massive wage disparities. Because our system taxes the individual rather than the family unit, a couple where one person earns $150,000 and the other earns $0 will pay thousands of dollars more in taxes than a couple where both earn $75,000.

The Canada Revenue Agency (CRA) does not offer many ways to fix this imbalance. But they do offer one massive, fully legal loophole: The Spousal RRSP.

If you are the primary breadwinner in your household, opening a standard personal RRSP is only solving half your problem. You are deferring your taxes today, but you are building a massive tax bomb for yourself in retirement. A Spousal RRSP changes the math entirely. It allows you to take a tax deduction at your high tax rate today, while ensuring the money is taxed at your partner’s much lower tax rate in the future.

This is the Official 2026 Guide to Spousal RRSPs. We will break down exactly whose contribution room is used, the "Age 71 Loophole" that extends your investing lifespan, and the critical "3-Year Attribution Warning" that catches thousands of Canadians off guard every tax season.

1. How a Spousal RRSP Actually Works (The Mechanics)

Who contributes, who gets the tax break, and who owns the money?

To use a Spousal RRSP correctly, you have to understand the three distinct roles in the transaction: the Contributor, the Annuitant, and the CRA.

The Setup

Let's assume a standard scenario: Alex earns $130,000 a year (High Earner). Jordan earns $30,000 a year (Low Earner).

Alex is paying a massive amount of income tax. Jordan is paying very little.

- The Account: Jordan opens a "Spousal RRSP" at the bank. Jordan is the Annuitant (the owner).

- The Contribution: Alex deposits $10,000 into Jordan's Spousal RRSP. Alex is the Contributor.

- The Tax Deduction: When tax season arrives, Alex claims the $10,000 deduction on their tax return. Because Alex is in a high tax bracket (approx. 43% in Ontario), this generates a massive tax refund of roughly $4,300.

- The Ownership: The moment the money enters the account, it belongs entirely to Jordan. In the event of a divorce, it is Jordan's money.

- The Withdrawal (The Goal): In retirement, when Jordan withdraws the money, it is added to Jordan's taxable income, not Alex's. Since Jordan is historically in a lower tax bracket, the household pays significantly less tax overall.

This strategy is the ultimate form of Income Splitting. You are shifting wealth from the high-taxed partner to the low-taxed partner, subsidized by the government.

2. The "Attribution" Warning: Surviving the 3-Year Rule

This is the most dangerous trap in Canadian retirement planning. Do not make a withdrawal until you understand this math.

The CRA knows that Spousal RRSPs are incredibly powerful. To stop people from abusing the system—for example, a high-earning spouse depositing $20,000 in December and the low-earning spouse withdrawing it in January to fund a vacation at a lower tax rate—the CRA created the Attribution Rule.

Also known as the 3-Year Rule, this is a strict time-lock on your money.

How the 3-Year Rule Works

If the Annuitant (the lower-earning spouse) withdraws money from a Spousal RRSP, the CRA will check to see if the Contributor (the higher-earning spouse) has deposited any money into any Spousal RRSP in the current calendar year or the two previous calendar years.

If the answer is YES: The withdrawal is "attributed" back to the high-earning Contributor.

The Penalty: The high earner must add the withdrawal to their taxable income for the year, and they are taxed at their high marginal rate. The income splitting strategy is completely destroyed.

The "Last-In, First-Out" (LIFO) Trap

The CRA does not track individual dollars; they look at the timeline. If you deposit money, the clock resets.

The Calculation Timeline (A Real-World Example):

Let's say Alex contributes $5,000 to Jordan's Spousal RRSP every year.

- Contribution 1: $5,000 deposited in 2022.

- Contribution 2: $5,000 deposited in 2023.

- Contribution 3: $5,000 deposited in 2024.

- Contribution 4: $5,000 deposited in 2025.

It is now 2026. Jordan wants to withdraw the $5,000 that was deposited way back in 2022. Jordan thinks, "It has been four years since that specific money went in, so it's safe."

Jordan is wrong.

Because Alex made a contribution in 2025 (the preceding year) and 2024 (two years preceding), the 3-Year Rule is triggered. If Jordan withdraws $5,000 in 2026, that $5,000 is attributed back to Alex and taxed at Alex's 43% rate. Before making any moves, always run your numbers through an RRSP Withdrawal Tax Calculator 2026 to see the devastating impact of an attribution error.

How to Beat the 3-Year Clock (The December Trick)

The CRA measures the 3-Year Rule in calendar years, not in months or days. This creates a massive loophole for savvy investors.

The rule looks at the Year of Withdrawal, minus the Year of Contribution, minus the Two Preceding Years.

To safely withdraw money in 2026, the absolute last contribution Alex could have made was on December 31, 2023.

- Year of Withdrawal: 2026

- Preceding Year 1: 2025 (No contributions allowed)

- Preceding Year 2: 2024 (No contributions allowed)

- Safe Year: 2023

The December vs. January Trap:

If Alex contributes $10,000 on December 31, 2023, that money clears the attribution rule on January 1, 2026. (Total wait time: 2 years and 1 day).

If Alex waits just 24 hours and contributes $10,000 on January 1, 2024, that money does not clear the attribution rule until January 1, 2027. (Total wait time: 3 full years).

This is why tax planners emphasize the end of the calendar year over the traditional "First 60 Days" RRSP deadline. If you are using a Spousal RRSP and foresee needing the money soon, always make your deposits in December, not January or February.

Exceptions to the Attribution Rule

The CRA will waive the 3-Year Rule and allow the lower-earning spouse to take the tax hit immediately only under very specific, usually tragic, circumstances:

- Death: The contributor dies in the year of the withdrawal.

- Divorce: The couple is living separate and apart due to a breakdown of the relationship at the time of the withdrawal.

- Non-Residency: The contributor or the annuitant is a non-resident of Canada for tax purposes at the time of the withdrawal.

- Conversion: The Spousal RRSP is converted into a Spousal RRIF, and only the "Minimum Mandatory Payment" is withdrawn. (Any excess withdrawal still triggers attribution).

3. Contribution Limits for 2026: Whose Room Is It?

Do not accidentally overcontribute and face the 1% monthly penalty.

The single most confusing aspect of the Spousal RRSP is understanding whose contribution limit is being used.

The Golden Rule: It is always the Contributor's room.

If Alex (High Earner) deposits money into Jordan's (Low Earner) Spousal RRSP, the CRA deducts that amount from Alex's personal RRSP contribution limit. Jordan's personal RRSP limit remains completely untouched.

- The 2026 Maximum: The maximum RRSP contribution limit for 2026 is $33,810 (or 18% of your earned income from 2025, whichever is lower).

- The Shared Pool: If Alex has $30,000 of contribution room in 2026, Alex can put $30,000 into their personal RRSP, OR $30,000 into Jordan's Spousal RRSP, OR split it ($15,000 each). Alex cannot put $30,000 in both.

To find your exact available room, look for your 2025 Notice of Assessment. If you file electronically and can't find your documents, use your CRA Netfile Access Code to log into the CRA portal securely and check your "Deduction Limit" line.

4. The "Age 71" Loophole: Extending Your Tax Deductions

How to keep getting tax refunds after the CRA says you have to stop.

According to Canadian tax law, your personal RRSP expires on December 31st of the year you turn 71. At that point, you must cash it out, buy an annuity, or convert it to a Registered Retirement Income Fund (RRIF) and begin forced withdrawals. You can never contribute to your personal RRSP again.

But what if you are 72, still working (or earning rental/business income), still paying high taxes, and still generating new RRSP contribution room?

The Solution: If your spouse is younger than 71, you can use the Spousal RRSP loophole.

Even though Alex is 72 and their personal RRSP is closed, Alex can still use their accumulated contribution room to deposit money into Jordan's Spousal RRSP (since Jordan is only 65).

- The Benefit: Alex gets to claim the tax deduction to lower their current high tax bill.

- The Result: The money goes to Jordan, who won't be forced to convert the account to a RRIF until Jordan turns 71 (six years from now). This allows the capital to continue growing tax-free for nearly a decade longer than the CRA intended.

5. The First-Time Home Buyer (HBP) Double-Up Strategy

How to extract $120,000 tax-free from your RRSPs.

The Home Buyers’ Plan (HBP) allows first-time buyers to withdraw up to $60,000 from their RRSP tax-free to buy a qualifying home, provided they pay it back over 15 years.

If you are a couple, you can each withdraw $60,000 from your respective RRSPs, for a total of **$120,000** towards your down payment.

But what if the high-earning spouse has $100,000 in their RRSP, and the low-earning spouse has $0? You can only access $60,000 total.

The Spousal RRSP Fix:

- Alex (High Earner) deposits $60,000 into Jordan's (Low Earner) Spousal RRSP.

- Alex gets a massive $60,000 tax deduction, resulting in a huge tax refund that can also be used for the house.

- The 90-Day Rule: As long as the money sits in the Spousal RRSP for at least 90 days, Jordan can withdraw it under the Home Buyers' Plan.

- The Attribution Bypass: Crucially, an HBP withdrawal does not trigger the 3-Year Attribution Rule. The CRA waives the penalty because the HBP is technically a loan to yourself, not taxable income.

This is the fastest, most tax-efficient way for a single-income family to generate a massive six-figure down payment in Canada today.

6. How to Set Up and Claim the Spousal RRSP

Do not accidentally open a regular RRSP.

When you go to the bank or log into Wealthsimple/Questrade, you must specifically open an account labelled "Spousal RRSP." If Alex just e-transfers $10,000 to Jordan's regular bank account and Jordan puts it in their own personal RRSP, the strategy fails. Jordan will get the tax deduction (which is useless since their income is low), and Alex gets nothing.

Filing Your 2026 Taxes:

When you get your contribution slip in the mail, it will have two names on it:

- Contributor: Alex (The person claiming the deduction on Schedule 7).

- Annuitant: Jordan (The person who owns the account).When Alex files their taxes, they will enter the amount on the line specifically designated for "Contributions to a spouse's or common-law partner's RRSP."

Frequently Asked Questions (FAQ)

Q: Can we transfer money from my regular RRSP to a Spousal RRSP?

A: No. You cannot convert your existing personal RRSP into a Spousal RRSP. A Spousal RRSP must be funded with "new" money (cash or in-kind transfers from a non-registered account). If you want to move funds, you must withdraw from your personal RRSP (paying the tax) and then contribute to the Spousal RRSP.

Q: What happens to the Spousal RRSP if we get divorced?

A: The money belongs to the Annuitant (the lower-earning spouse). However, during divorce proceedings, RRSPs are generally considered "family property" and are subject to a 50/50 split during the equalization of net family property. The CRA allows a tax-free rollover of RRSP funds between spouses under a formal separation agreement (Form T2220).

Q: Does a Spousal RRSP affect my TFSA?

A: No. The RRSP and the Tax-Free Savings Account are completely separate systems. Contributing to a Spousal RRSP does not use up any of your (or your partner's) TFSA contribution room. If you are debating which account to fund first, ensure you understand which sources of your income are actually taxable by reviewing our Non-Taxable Income Sources in 2026 guide.

Q: Can a common-law partner open a Spousal RRSP?

A: Yes. The CRA treats common-law partners exactly the same as married couples for the purpose of Spousal RRSPs. You must meet the CRA definition of common-law (living together in a conjugal relationship for at least 12 continuous months, or having a child together).

About the Author

Jeff Calixte (MC Yow-Z) is a Canadian career researcher and digital entrepreneur who studies hiring trends, labour market data, and real entry-level opportunities across Canada. He specializes in simplifying the job search for newcomers, students, and workers using practical, up-to-date information.

Sources

- Canada Revenue Agency: Contributing to a Spousal or Common-Law Partner RRSP

- CRA: Withdrawing from Spousal RRSPs (Attribution Rules)

- Department of Finance: Income Splitting and Pension Regulations

Note

Job availability, wages, and hiring conditions can vary widely by province, employer, season, and experience level. All salary ranges and job examples in this guide are estimates based on current labour market data. Always confirm details directly with the employer before applying.